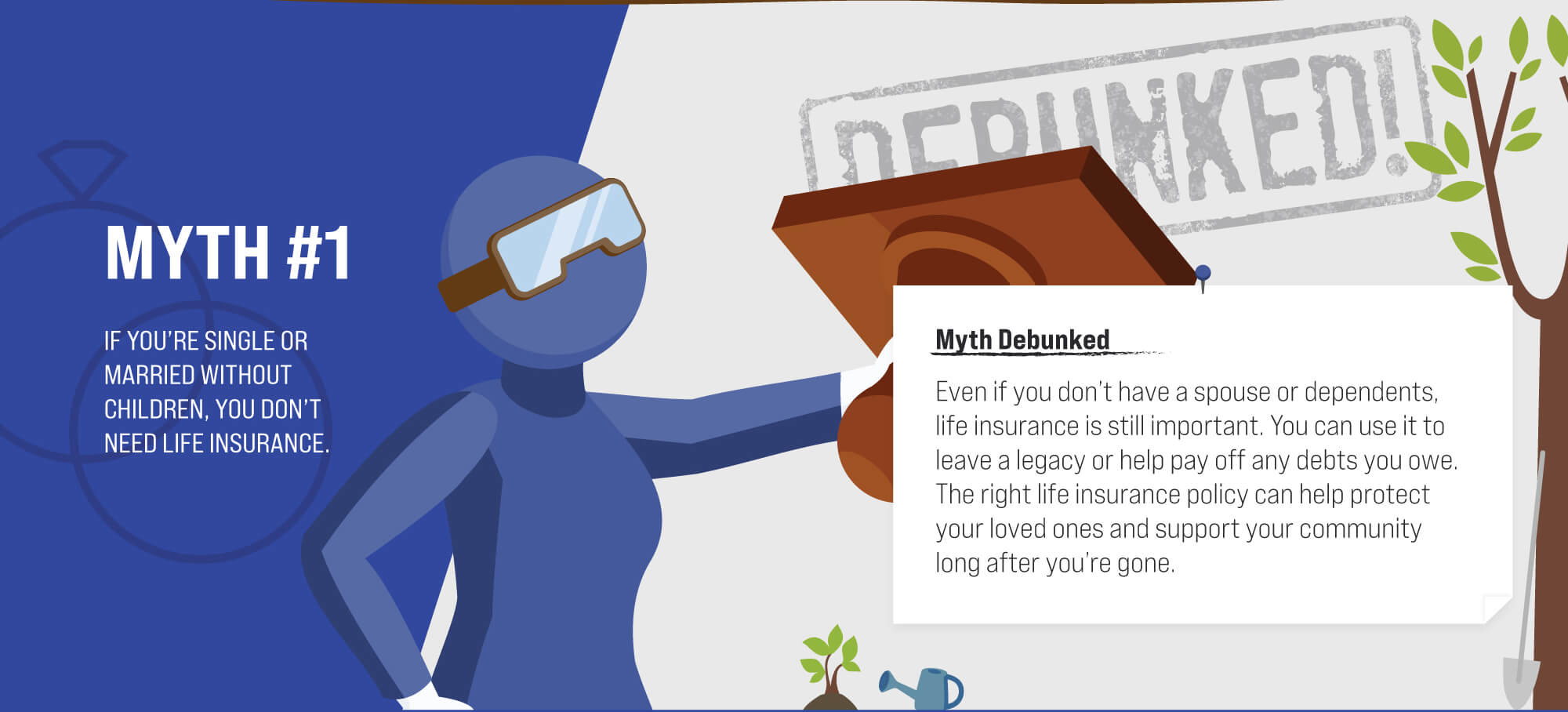

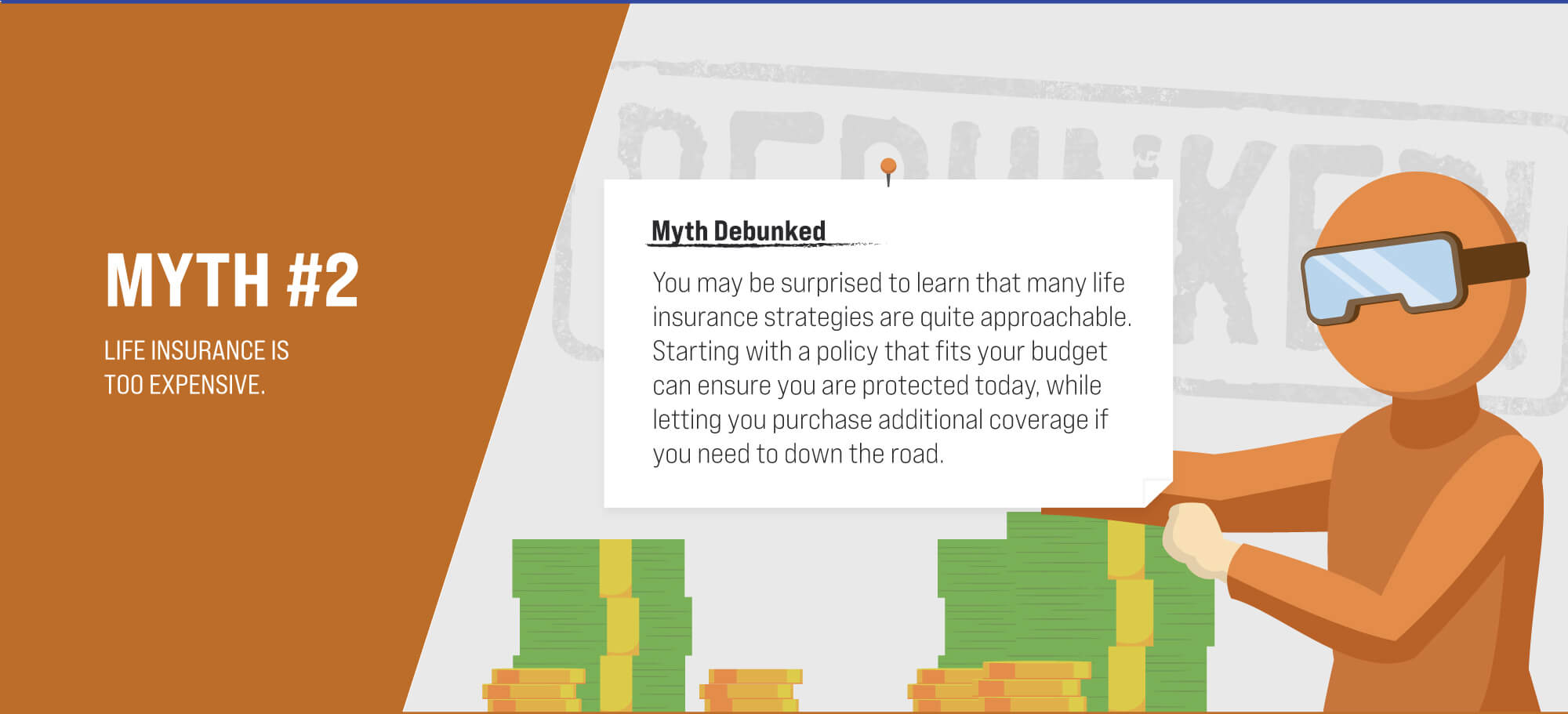

Life Insurance Myths: Debunked

Whole life insurance remains in force as long as you remain current with premiums. Here's how it works.

Solve a mystery while learning how important your credit report is with this story-driven interactive.

Have you found yourself suddenly single? Here are 3 steps to take right now.